Securing a business loan can be a crucial step for start-ups looking to grow, develop products, or enter new markets. However, borrowing money as a start-up can be challenging, given the lack of financial history and the inherent risks of new ventures. In this guide, we’ll explore the key factors you should consider before taking out a business loan for your start-up and how to ensure the loan works in your favor rather than becoming a financial burden.

1. Understand Your Financing Needs

Before applying for a loan, the first step is to clearly understand how much funding your start-up requires and how those funds will be allocated. Lenders will want to know that you have a solid plan in place. Break down your financing needs into categories:

- Operational costs: How much do you need for day-to-day operations?

- Product development: If you are building a product, how much will it cost to bring it to market?

- Marketing: What is your budget for customer acquisition and marketing campaigns?

- Staffing: How many employees do you need, and how much will payroll cost?

Tip: Avoid borrowing more than you need. Excessive borrowing could result in unnecessary debt, which can strain your cash flow in the future.

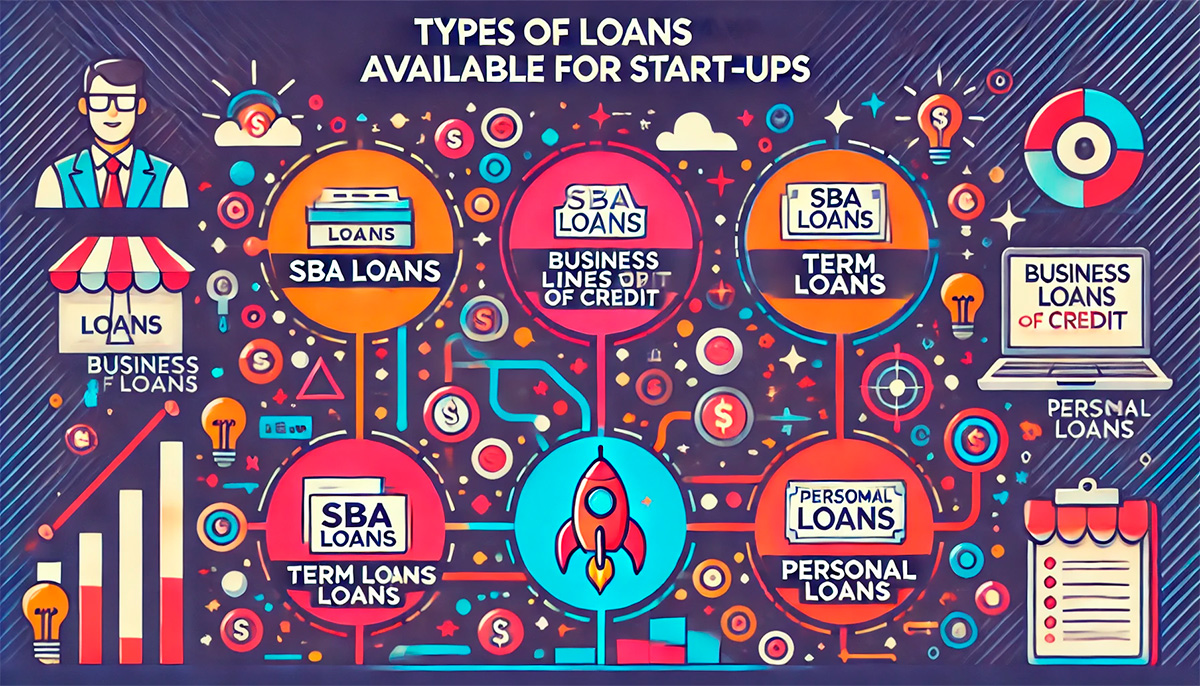

2. Types of Loans Available for Start-Ups

Not all loans are created equal, especially for start-ups. Some loans are more suitable for new businesses than others. Below are the most common loan types that might work for start-ups:

| Type of Loan | Advantages | Disadvantages |

|---|---|---|

| Small Business Administration (SBA) Loans |

|

|

| Business Lines of Credit |

|

|

| Term Loans |

|

|

| Personal Loans for Business |

|

|

Tip: Weigh the pros and cons of each loan type to determine which aligns best with your start-up’s specific needs and your financial situation.

3. Assess Your Creditworthiness

Lenders will assess your creditworthiness, often looking at both your personal and business credit scores (if you have one). As a start-up, your personal credit score will likely play a larger role in the loan decision. Here’s how to assess and improve your creditworthiness:

- Check your credit report: Ensure there are no errors or inaccuracies that could hurt your score.

- Pay off debts: Reducing existing debt can boost your credit score and make you a more attractive borrower.

- Establish business credit: If possible, start building your business credit by using a business credit card responsibly.

Tip: If your credit score is less than ideal, you may still qualify for a loan by offering collateral or seeking a co-signer with a stronger credit profile.

4. Interest Rates and Loan Terms: Finding the Best Deal

It’s essential to compare interest rates and loan terms across multiple lenders before making a decision. Even a small difference in the interest rate can significantly impact the total cost of your loan over time. Pay close attention to the following:

- Interest rates: Fixed or variable? Compare the rates offered and calculate how much you’ll pay over the life of the loan.

- Loan term: How long do you have to repay the loan? Longer terms may mean smaller payments but more interest paid overall.

- Fees: Are there origination fees, prepayment penalties, or closing costs? Be sure to understand all associated fees before agreeing to a loan.

Tip: Use online calculators to estimate the total cost of the loan based on different interest rates and loan terms. This can help you make an informed decision about which option is best for your start-up.

5. Risks of Taking Out a Loan as a Start-Up

While loans can provide crucial funding, they also come with risks, especially for start-ups. Consider the following risks:

- Repayment pressure: Start-ups often experience unpredictable revenue streams. Ensure your start-up can comfortably meet loan repayments, even during periods of slow growth.

- Collateral risk: If the loan requires collateral, such as property or equipment, you risk losing these assets if your business cannot meet the repayment terms.

- Debt burden: Taking on too much debt early on can limit your start-up’s financial flexibility and increase the pressure to generate immediate revenue.

Tip: Before taking out a loan, perform a stress test on your finances. Assess how your start-up would handle loan repayments during a worst-case scenario, such as a slow sales period or delayed product launch.

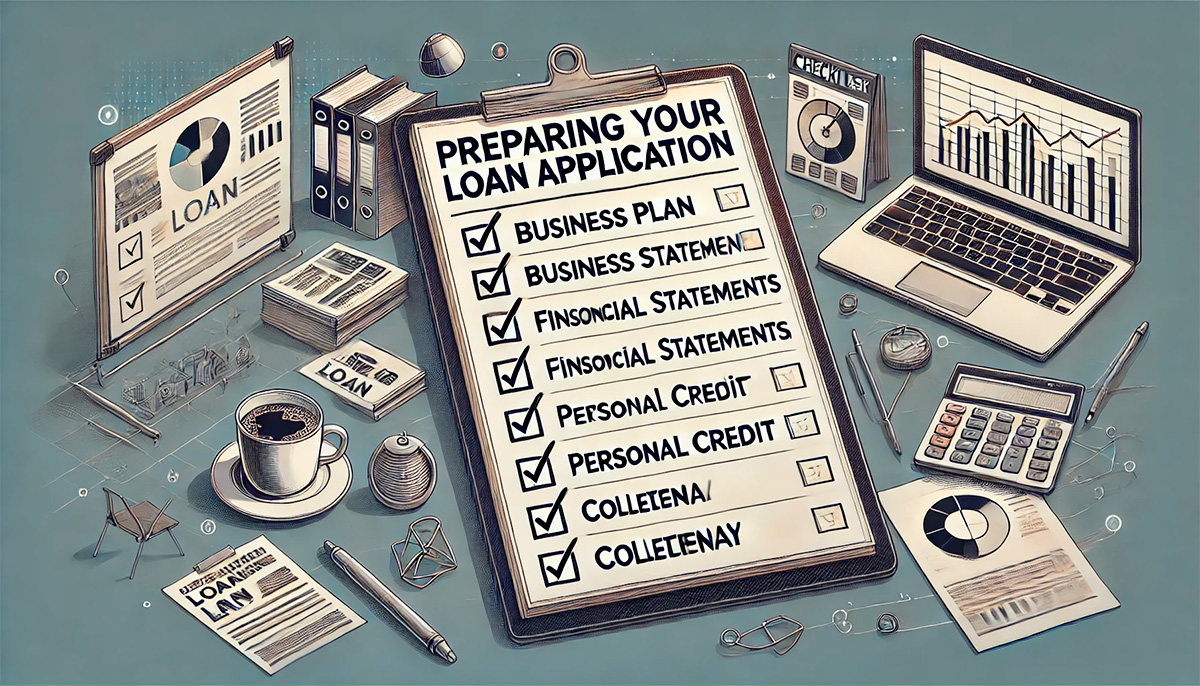

6. Preparing Your Loan Application

To increase your chances of approval, it’s essential to prepare a strong loan application that demonstrates the potential of your start-up. Here’s what lenders will look for:

- Business Plan: A detailed business plan that outlines your goals, market strategy, financial projections, and how you intend to use the loan.

- Financial Statements: Current financial information, such as profit and loss statements, cash flow reports, and balance sheets (if available).

- Personal Financial Information: For start-ups, lenders may request personal tax returns, credit reports, and bank statements.

- Collateral: If the loan requires collateral, be prepared to show documentation of the assets you’re willing to offer.

Tip: Take the time to polish your business plan and financial statements. The more organized and detailed your loan application, the more likely you are to be approved.

Conclusion: Making the Right Decision for Your Start-Up

Securing a business loan can provide the capital your start-up needs to grow, but it’s essential to weigh the benefits and risks carefully. By understanding your financial needs, evaluating the loan types available, and preparing a solid loan application, you can increase your chances of obtaining financing that aligns with your business goals.

Always remember, taking on debt is a serious commitment, and it’s crucial to ensure that your start-up is financially ready for the responsibility. A well-chosen loan can be the springboard for success, but it should always be approached with caution and thorough planning.